Medicare’s Nursing Home Coverage

Medicare Part A covers institutional care in hospitals and skilled nursing facilities, as well as certain care given by home health agencies and care provided in hospices.

Any person who has reached age 65 and who is entitled to Social Security benefits is eligible for Medicare Part A without charge. That is, there are no premiums for this part of the Medicare program.

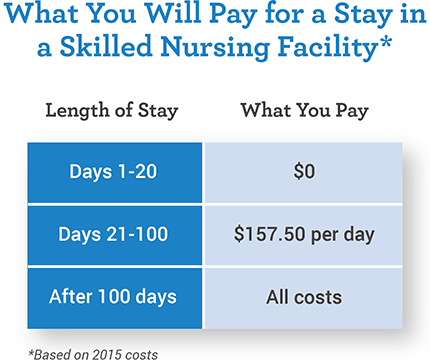

Medicare Part A covers up to 100 days of “skilled nursing” care per illness. However, the conditions for obtaining Medicare coverage of a nursing home stay are quite stringent.

Here are the main requirements:

- The Medicare recipient must enter the nursing home no more than 30 days after a hospital stay (meaning admission as an inpatient; “observation status” does not count) that itself lasted for at least three days (not counting the day of discharge).

- The care provided in the nursing home must be for the same condition that caused the hospitalization (or a condition medically related to it).

- The patient must receive a “skilled” level of care in the nursing facility that cannot be provided at home or on an outpatient basis. In order to be considered “skilled,” nursing care must be ordered by a physician and delivered by, or under the supervision of, a professional such as a physical therapist, registered nurse or licensed practical nurse. Moreover, such care must be delivered on a daily basis. (Few nursing home residents receive this level of care.)

- As soon as the nursing facility determines that a patient is no longer receiving a skilled level of care, the Medicare coverage ends. And, beginning on day 21 of the nursing home stay, there is a significant copayment equal to one-eighth of the initial hospital deductible ($157.50 a day in 2015). This copayment will usually be covered by a Medigap insurance policy, provided the patient has one or there pay be a different copayment structure with a Medicare Advantage plan (Part C).

A new spell of illness can begin if the patient has not received skilled care, either in a skilled nursing facility (SNF) or in a hospital, for a period of 60 consecutive days. The patient can remain in the SNF and still qualify as long as he or she does not receive a skilled level of care during that 60 days.

Nursing homes often terminate Medicare coverage for SNF care before they should. Two misunderstandings most often result in inappropriate denial of Medicare coverage to SNF patients. First, many nursing homes assume in error that if a patient has stopped making progress towards recovery then Medicare coverage should end. In fact, if the patient needs continued skilled care simply to maintain his or her status (or to slow deterioration) then the care should be provided and is covered by Medicare.

Second, nursing homes may wrongly believe that care requiring only supervision (rather than direct administration) by a skilled nurse is excluded from Medicare’s SNF benefit. In fact, patients often receive an array of treatments that don’t need to be carried out by a skilled nurse but that may, in combination, require skilled supervision. In these instances, if the potential for adverse interactions among multiple treatments requires that a skilled nurse monitor the patient’s care and status, then Medicare will continue to provide coverage.

Second, nursing homes may wrongly believe that care requiring only supervision (rather than direct administration) by a skilled nurse is excluded from Medicare’s SNF benefit. In fact, patients often receive an array of treatments that don’t need to be carried out by a skilled nurse but that may, in combination, require skilled supervision. In these instances, if the potential for adverse interactions among multiple treatments requires that a skilled nurse monitor the patient’s care and status, then Medicare will continue to provide coverage.

When a patient leaves a hospital and moves to a nursing home that provides Medicare coverage, the nursing home must give the patient written notice of whether the nursing home believes that the patient requires a skilled level of care and thus merits Medicare coverage. Even in cases where the SNF initially treats the patient as a Medicare recipient, after two or more weeks, often, the SNF will determine that the patient no longer needs a skilled level of care and will issue a “Notice of Non-Coverage” terminating the Medicare coverage.

Whether the non-coverage determination is made on entering the SNF or after a period of treatment, the notice asks whether the patient would like the nursing home bill to be submitted to Medicare despite the nursing home’s assessment of his or her care needs. The patient (or his or her representative) should always ask for the bill to be submitted. This requires the nursing home to submit the patient’s medical records for review to the fiscal intermediary, an insurance company hired by Medicare, which reviews the facilities determination.

The review costs the patient nothing and may result in continued Medicare coverage.

While the review is being conducted, the patient is not obligated to pay the nursing home. However, if the appeal is denied, the patient will owe the facility retroactively for the period under review. If the fiscal intermediary agrees with the nursing home that the patient no longer requires a skilled level of care, the next level of appeal is to an Administrative Law Judge. This appeal can take a year and involves hiring a lawyer. It should be pursued only if, after reviewing the patient’s medical records, the lawyer believes that the patient was receiving a skilled level of care that should have been covered by Medicare. If you are turned down at this appeal level, there are subsequent appeals to the Appeals Council in Washington, and then to federal court.

While the review is being conducted, the patient is not obligated to pay the nursing home. However, if the appeal is denied, the patient will owe the facility retroactively for the period under review. If the fiscal intermediary agrees with the nursing home that the patient no longer requires a skilled level of care, the next level of appeal is to an Administrative Law Judge. This appeal can take a year and involves hiring a lawyer. It should be pursued only if, after reviewing the patient’s medical records, the lawyer believes that the patient was receiving a skilled level of care that should have been covered by Medicare. If you are turned down at this appeal level, there are subsequent appeals to the Appeals Council in Washington, and then to federal court.If you need legal assistance you can contact the following elder law attorney’s in your state.

Elder Law Offices in Maine

| Maine Center for Elder Law www.mainecenterforelderlaw.com |

Maine Elder Law Firm www.maineelderlaw.com |

| Portland Office: One Monument Way, 2nd Floor Portland, ME 04101 Phone: 207-619-2529 |

Bangor Office: 33 Mildred Avenue Bangor, Maine 04401 Phone: 207-947-6500 |

| Kennebunk Office: 3 Webhannet Place, Suite 1 Kennebunk, ME 04043 Phone: 207-467-3301 |

Click here to find a law office in your area.

Find Elder Law Offices in New Hampshire

I would be happy to answer any questions you might have about this, or any other Health Insurance topic. I can be reached at 207-370-0143 or at http://www.mainemedicareoptions.com/contact