“What’s the differences between Medicare Supplements and Medicare Advantage?”

Questions like this are the reason I do what I do. You need to know what your options are in Maine when you turn age 65 and enroll in Medicare – and there are a lot of options!

There are many differences between Medicare Supplement plans or Medigap as they are called in the Medicare literature.

One difference between Medigap and Medicare Advantage plans is that Medicare Advantage contracts operate on a calendar year basis and can have changes from year to year just like the health insurance plan you had prior to Medicare. Medicare Supplement policies are standardized and are the same year after year.

Another difference is the cost. Medicare Advantage Plans generally have much lower monthly premiums (sometimes $0) And some Medicare Advantage plans pay you! (Yes you read that right!) Medigap plans can cost much more, often in the $200/month range.

With Medicare Advantage plans you are required to share in your medical costs by paying co-pays as you use the plans. These plans operate very similar to the Medical insurance you may have had before you retired if you had an HMO or a PPO plan on the Healthcare marketplace (Obamacare) or with an employer. Most Medigap plans have very small out of pocket costs while they cost much more up front.

This is why most people turning 65 or planning retirement choose to meet with someone like myself who has the knowledge and experience with the different plans and can help you decide which plan is best for you. Choosing between these two types of Medicare insurance plans is just the first step.

Once you’d decided on Medigap or Medicare Advantage then you must choose which Medigap plan or which Medicare Advantage plan best fits your needs. You may also need to pick a separate Part D prescription drug plan if the plan you choose does not include drug coverage.

Also, the best plan for you may not always be the best plan for your spouse so you will have to do the same research for both of you. I can explain everything you need to know so that you can make the best choice. You can schedule a meeting quickly and easily using this button.

If you have a question that needs to be answered right away, just give me a call. My number is (207) 370-0143 or call toll free 866-976-9038.

Want to know more?

If you would like help comparing your needs against the many Medicare plans out there or if you just want to ask a few questions, you can call me directly at 207-370-0143 or use my simple form on the CONTACT page of this site to send an email message.

The best part about working with me is that it will not cost you anything to talk with me to discuss your options and review the plans that are available. I am paid by the insurance companies in the form of a commission when you enroll in a plan. You will not pay anything to meet with me and you will pay the same price for your insurance that everyone pays whether they had my help or not.

“My goal is to help people and I have found great joy in being able to offer my services to people who need my help.”

Learn how your VA Benefits and Original Medicare work

VA Benefits and Medicare: What You Need to Know

As a Medicare-eligible Veteran, you have more options when it comes to healthcare. The transition to Medicare can be confusing, so this article will list a few points that all vets should know when they become Medicare eligible. To confirm your options call the Veterans Administration directly at 1-877-222-VETS (8387).

VA Benefits and Medicare

It is important to know that Veteran’s (VA) plans and Medicare do not supplement each other. In other words: VA plans only cover care at VA facilities, and Medicare only covers care at Medicare assigned doctors and hospitals.

Should You Enroll in Medicare Part A If You Have VA Benefits?

Yes. You can have both Medicare and Veterans (VA) benefits at the same time. It is strongly recommended that all veterans enroll in Medicare Part A (Hospital Coverage) when they turn 65 and generally there is no additional cost for Part A. This will allow you receive hospital coverage should you go to a non-VA facility. According to the VA’s website “All Veterans are encourage you to enroll in Medicare health insurance.” Source: VA.gov

Should You Get Medicare Part B If You Have VA Benefits?

Yes, It is strongly recommended that all veterans enroll in Medicare Part B (Medical Coverage) as well as part A when they are eligible. (Click here to learn more about when to enroll.)

There is a monthly fee for Part B but it is worth it. If your VA Benefits are dropped at some point OR, and this is important, if your local VA facility does not cover all health services, you could pay 100% out of pocket for a serious illness.

The VA highly recommends that you enroll in Part B as well. Please contact Veterans Affairs directly (1-877-222-VETS (8387)) with questions about specific care at Togus or another local facility.

Should You Get a Medigap or Medicare Advantage If You Have VA Benefits?

If you would prefer to see a local doctor or go to a local hospital or healthcare facility for your care then you should consider a Medicare Advantage or Medigap plan to supplement your Medicare coverage. Read more about these types of plans here.

Most people agree that veterans do not need a Medigap plan if they qualify for ChampVA. However, if you aren’t enrolled in ChampVA, a Medigap plan will fill in the gaps such as deductibles, copays, and coinsurance, as well as other benefits when seeking care outside of the VA, or outside of the U.S. and its territories.

Make sure to speak with one of our agents before enrolling in any supplemental plan to ensure that it is actually beneficial for you.

Here are two reasons why you may want to enroll in a private Medicare Supplement plan:

You do not live near a VA facility

You are enrolled in one of the VA lower priority groups, and could potentially lose your benefits

“There is no guarantee that in subsequent years Congress will appropriate sufficient funds for VA to provide care for all enrollment Priority Groups. This could happen if you are enrolled in one of the lower Priority Groups. This would leave you with no health care coverage.” Source: VA.gov

The choice of whether to enroll in Part D is up to you. In most cases, you don’t need a Medicare Prescription Drug Plan, aka Medicare Part D, as VA plans may offer more coverage than Medicare’s Rx coverage.

Remember that any prescription prescribed by a non-VA doctor needs to be approved by your VA doctor for the VA to cover it. This may take extra time and your VA doctor can say that prescription is unnecessary. Many veterans use a Medicare Advantage plan as a back up because they don’t cost you any extra. [READ MORE]

What about the Part D Penalty?

Good news! Your VA drug coverage is considered creditable coverage so the Part D late enrollment penalty does not apply to you. If you choose not to enroll in Part D when you are first eligible you can still enroll later on in Part D without paying a penalty.

For further questions about Medigap, Medicare Advantage or Medicare Part D, please call (207) 370-0143 or schedule a phone call to discuss your options.

Medicare uses information from member satisfaction surveys, plans, and health care providers to give overall performance star ratings to plans.

A plan can get a rating between 1 and 5 stars. A 5-star rating is considered excellent. These ratings are designed to help you compare plans based on quality and performance.

NOTE: You can only switch to a 5-star Medicare Advantage Plan, Medicare Cost Plan, or Medicare Prescription Drug Plan one time before November 30 each year.

If you move from a Medicare Advantage Plan that includes prescription drug coverage to a stand-alone Medicare Prescription Drug Plan, you’ll be disenrolled from your Medicare Advantage Plan, including the health benefit. You’ll be returned to Original Medicare for coverage of your health services. You can only switch to a 5-star Medicare Prescription Drug Plan if one is available in your area.

If you move from a Medicare Advantage Plan that has drug coverage to a 5‑star Medicare Advantage Plan that doesn’t, you may lose your prescription drug coverage. You’ll have to wait until your next enrollment opportunity to get drug coverage, and you may have to pay a Part D late enrollment penalty.

5-star plans are identified with this special icon:

How to compare plans using the Medicare Star Rating System

Part D drug plans and Medicare Advantage Plans vary greatly in terms of costs and coverage. Each year plans can change their coverage and costs for the new calendar year. This means that every year you should review your plan’s coverage and compare it with other plans in your area to make sure you have the coverage that is best for you.

If you’re working with an agent you can ask them to help you review your options. If you are doing it alone then you’ll have to examine each new plan’s coverage, costs, drug coverage, and the pharmacies in its network to see if it best meets your current needs.

After considering all these important factors to narrow down your choices, you can use the plan’s star rating from Medicare to help you make a final decision.

Medicare Advantage Plans are rated on how well they perform in five different categories:

Staying healthy: screenings, tests, and vaccines

Managing chronic (long-term) conditions

Plan responsiveness and care

Member complaints, problems getting services, and choosing to leave the plan

Health plan customer service

Part D plans are rated on how well they perform in four different categories:

Drug plan customer service

Member complaints, problems getting services, and choosing to leave the plan

Member experience with the drug plan

Drug pricing and patient safety

REMEMBER: Before you consider a plan’s star rating, make sure the plan’s coverage and costs suit your needs. For example, if you are considering a Part D plan, be sure the new plan covers your drugs at a cost that works for you.

Where can I find information on my plan’s star rating?

Star ratings can be found using Medicare’s Plan Finder tool or by calling 1-800-MEDICARE. New plan quality ratings come out each October and apply to the next calendar year (for example, plan ratings for 2021 will be available in November 2020).

How can I use the star ratings to inform my plan choice next year?

You can use star ratings to compare plans in your service area by the categories listed above that Medicare finds important indicators of the insurance company’s performance. Remember that a plan’s star rating is only one factor to look at when comparing plans. Even though a plan has a high star rating, it may not be right for you. You should also consider the plan’s costs, coverage, and network for providers and pharmacies.

TIP

Working with an agent can save you time and money. Agents have experience with the insurance companies that offer plans in the local area. Agents can give you important feedback on which plans their clients are happiest with and will also update you each year on important changes. Best of all, working with an agent costs you nothing.

If Medicare gives a plan fewer than three stars for three years in a row, It will be flagged as as low-performing. The symbol Medicare uses to show that a plan is low-performing is an upside-down red triangle with an exclamation point inside of it (similar to a caution sign).

Medicare will notify you if the plan you are enrolled in is flagged as low-performing. You will not be removed from the plan, but you may want to check the plan’s costs and coverage to make sure it is still a good plan for you.

What is the Five-Star Special Enrollment Period?

Generally, you can only change your plan or enroll in a new plan during specific times. Special Enrollment Periods (SEP) are periods of time outside normal enrollment periods, triggered by specific circumstances.

If you want to enroll in a plan or change plans, you can take advantage of an SEP to join or switch to a five-star Medicare Advantage or Part D plan. This means that you can enroll in a Medicare Advantage Plan or stand-alone Part D plan in your service area that has an overall plan performance rating of five stars. You may only use this SEP once per calendar year.

This SEP begins December 8 of the year before the plan is considered a five-star plan (remember that ratings come out in November) and lasts through November 30 of the year the plan is a five-star plan

Enrollments in December are effective January 1

Enrollments from January to November are effective the month following the enrollment request

Want to know more?

If you would like to talk to me or schedule a meeting, you can reach me at 207-370-0143 or use the simple form below to send an email message.

The best part about working with me is that it will not cost you anything to discuss your options or to review the plans that are available. I am paid by the insurance companies in the form of a commission if you enroll in a plan. Just like your car insurance agent!

I will help you shop around to find the plan with the best price and the most benefits. My goal is to help you and I have found great joy in being able to offer my services to people who need my help.Shortcode

If you are turning 65 this year or retiring, you may have questions.

Call me today and I will be happy to explain all your options and help you compare plans so you can choose the coverage you need for a price you can afford.

Schedule a phone call or an in-person meeting.

I can answer all your questions over the phone or we can meet face-to-face and I can help you with everything you need to know. I have all the forms and applications you need and I can also help you complete them.

Clinics offering low-cost or free dental care in Maine

Androscoggin County

Auburn: CCS Dental Clinic, 207-755-3456 Open: Monday – Thursday, 7:00-6:00; Friday, 7:00-5:00; October—May, 1st Saturday, 8:00-4:30 Serves: Children 18 & younger with MaineCare or uninsured Cost: Sliding-scale fees; accepts MaineCare

Lewiston: Community Dental, 207-777-7442 Open: Monday – Friday, 8:00-4:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Turner: DFD Russell Health Center, 207-225-2676 Open: Call for availability Serves: Current patients of the Health Center Cost: Sliding-scale fees; accepts MaineCare

Aroostook County

Houlton: Katahdin Valley Dental Center, 1-866-366-5842 Open: Monday – Friday, 7:30-5:30 Serves: Residents of Ashland, Brownville, Houlton, Millinocket,

Eagle Lake: Eagle Lake Health Center 207-444-3012 Open: Monday and Tuesday, 7:00-5:30; Tuesday 8:00-7:00; Thursday, 7:00-5:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Fort Kent: Bolduc Avenue Health Center 207-728-3119 Open: Mon, Tues, Thur, Fri 9:00 – 5:00 Wed. 12:00—5:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Madawaska: Madawaska Community Health Center, 207-728-3119 Open: Thursday, 7:00-5:30 and Friday, 7:00-5:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare; private insurance

Presque Isle: St. Apollonia Dental Clinic, 207-554-5045 Open: Monday – Thursday, 7:30-4:30 Serves: Children up to 21st birthday Cost: Sliding-scale fees; accepts MaineCare, private insurance

Cumberland County

Portland: Community Dental, 207-874-1028 Open: Monday – Friday, 8:00-4:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Portland: Greater Portland Health, 207-874-2141 Open: Varies by location; call for specific hours at each Serves: Patients of Greater Portland Health and children in Portland schools Cost: Sliding-scale fees; accepts MaineCare, private insurance

Portland: University of New England Oral Health Center, 207-221-4747 Open: Year-round, dentures and general oral care, call for available times Serves: Greater North New England; all ages Dental Hygiene Clinic Open: Monday-Friday, 8:00-4:00, September through April Cost: Discounts and reduced fees; accepts MaineCare, Delta Dental; call for other insurances

Portland: The Root Cellar Dental Clinic, 207-774-3197 Open: Call for appointment Serves: Adults and children living in Portland’s East End Cost: No cost for general services; fees for denture and lab work

Franklin County

Farmington: Community Dental, 207-779-2659 Open: Monday – Friday, 8:00-4:30 Serves: Residents of Franklin County and areas without a closer Community Dental location Cost: Sliding-scale fees; accepts MaineCare, private insurance

Strong: Strong Area Dental Health Center, 207-684-3045 Open: Monday, 7:00-6:00; Tuesday-Thursday, 7:00-4:30; closes for lunch 12:15–12:45 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Hancock County

Bucksport: Regional Dental Center, 207-902-1100 Open: Monday – Thursday, 7:30-5:00 Serves: Bucksport region, Hancock, Penobscot, Waldo, and Washington County Cost: Sliding-scale fees; accepts MaineCare, private insurance

Southwest Harbor: Community Dental Center, 207-244-2888 Open: Monday – Thursday, 8:00-5:00 Friday, 8:00-noon Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Kennebec County

Augusta: Kennebec Valley Family Dentistry, 207-623-3400 Open: Monday – Thursday, 8:00-4:00; Friday, 8:00-4:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Monmouth: DFD Russell, 207-933-9646, hygienist only, no dental staff Open: Call for available times Serves: Current DFD patients only, dental hygiene only Cost: Sliding-scale fees; accepts MaineCare for pediatric patients

Waterville: Community Dental Center, 207-872-8891 Open: Monday – Thursday, 7:30– 5:00 (closed for lunch 1:00-1:40 daily) Serves: Kennebec and Somerset Counties, pediatric patients; adult patients should call for availability Cost: Sliding-scale fees; accepts MaineCare, private insurance

Knox County

Rockland: Knox County Health Clinic, 207-921-6996 Open: Call for application for an appointment Serves: Children and adults to age 55 and adults over 55 who are employed at least 20 hours per week in Knox County, Waldoboro, and Lincolnville Cost: Sliding–scale fees; accepts MaineCare

Vinalhaven: Islands Community Dental Services, 207-863-2533 Open: Wednesday-Thursday, 8:30-4:30; Fridays and Saturday, call for times Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Lincoln County

Damariscotta: Lincoln County Dental, 207-563-8668 Open: Monday – Friday, 8:00-4:30 Serves: Lincoln County residents, depending on availability Cost: Reduced fee for uninsured, low-income individuals

Oxford County

Rumford: Community Dental, 207-369-3600 Open: Monday – Friday, 8:00-4:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Penobscot County

Bangor: UMA, Bangor Campus Dental Hygiene Clinic, 207-262-7872 Open: Call for available times. This is not a year-round program. Serves: All Cost: Low fees, does not accept any insurance

Bangor: Penobscot Community Dental Center, 207-992-2152 Open: Monday – Friday, 7:30-6:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Dexter: Home Town Health Center Dental Services, 1-866-364-1366 or 207-924-5200 Open: Tuesday – Friday, 7:00-5:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Lincoln: Health Access Family Dental, 794-6700, Currently no dentist but taking names for a wait list Open: Monday – Thursday, 7:30-5:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Millinocket: Katahdin Valley Health Center Dental Clinic, 207-723-6565 Open: Monday – Thursday, 7:30-5:30 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Newport: Home Town Health Center Dental Services, 207-355-3521 Open: Monday—Thursday, 7:00-6:00 Serves: All Cost: Sliding-scale; MaineCare; private insurance accepted

Piscataquis County

See other counties, and look for the closest center to you that does not restrict their services to a certain geographic area.

Sagadahoc County

Bath: Jessie Albert Dental & Orthodontic Center, 207-443-9721 or 1-888-304-8020 Open: Monday – Thursday, 7:30-4:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Brunswick: Oasis Free Clinic, 207-721-9277 Open: Monday, 9:00-12:00; Friday, 8:00-12:00; 1st & 3rd Tuesday, 6:00-9:00 Serves: Oasis medical patients living in greater Brunswick, Bath, Freeport, Harpswell, Sagadahoc County and the Islands Cost: Free

Somerset County

Bingham: Bingham Area Dental Center, 207-672-3519 Open: Tuesday – Thursday, 7:00-4:30; Friday 7:00-4:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Waldo County

Belfast: Waldo County Dental Care, 207-338-9307 Open: Monday – Thursday, 8:00-3:00 Serves: Waldo County residents 18 years and older who have not seen a dentist in the last 12 months Cost: Sliding-scale fees, limited MaineCare

Washington County

Eastport: Eastport Health Care, 207-853-6001 Open: Monday – Friday, 8:00-5:00; Tuesday, 8:00-6:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance Harrington: Harrington Family Health Center, 207-483-4502 Open: Monday—Thursday, 8:00—5:00 Serves: All basic dentistry and dental hygiene Cost: Sliding-scale fees; accepts MaineCare, private insurance Lubec: Regional Medical Center, 207-733-5541 Open: Monday – Friday, 7:30-5:00; Serves: All Cost: Sliding-scale; accepts MaineCare, private insurance

York County

Bar Mills: Leavitt’s Mill Free Health Center, 207-929-6455 Not accepting new patients; closing permanently July 2019 Open: Tuesday-Friday, 9:00-4:00 Serves: Must be a health center patient; dental hygiene only Cost: Free Biddeford: Community Dental, 207-282-1305 Open: Monday– Friday, 8:00– 4:30 Serves: All Cost: Sliding-scale fee; accepts MaineCare, private insurance Springvale: Nasson Health Care, 207-490-6900 Open: Monday, Tuesday, Wednesday, Friday, 8:00-5:00; Thursday, 9:00-5:00 Serves: All Cost: Sliding-scale fees; accepts MaineCare, private insurance

Other Programs

Maine Donated Dental Services Program, 1-800-205-5615 Call for details, serves people ages 62 & up with dentists willing to offer discounted services. Currently closed to all counties except Hancock and Waldo unless medically compromised. Wait list is a year or more.

Tooth Protectors 207-513-1111 www.toothprotectors.org Serves all areas of Maine free for children 20 years and younger with MaineCare. Cost: Discounted fees; accepts MaineCare, private insurance

Maine Dental Health Out-Reach 207-377-7003 Serves children in: Androscoggin, Kennebec and Franklin counties and students in school districts including Augusta, MSAD 11, RSU2, RSU73 and Winthrop. Go to www.mdhoi.org for eligibility requirements.

Don’t live in Maine?

Click below to find a low-cost clinic in your state.

Most people don’t pay a monthly premium for Part A (sometimes called “premium-free Part A”). If you paid Medicare taxes for 40 or more quarters and you have earned your Social Security Benefit then you will not pay the Part A premium. You have earned it through your taxes.

However, if you paid Medicare taxes for less than 30 quarters, the standard Part A premium you will pay is $437.

If you paid Medicare taxes for 30-39 quarters, the standard Part A premium is $240.

Medicare Part B

The standard Part B premium amount for 2019 will increase by $1.50. The premium will increase from $134 to $135.50.

Medicare Deductibles

The annual deductible for all Part B beneficiaries will be $185.00 in 2019. However, depending on the insurance plan you choose, this deductible may be covered by your supplmental insurance plan.

The Medicare Part A annual deductible that beneficiaries pay when admitted to the hospital will be $1,364.00 in 2019.. The Part A deductible covers your share of costs for the first 60 days of Medicare-covered inpatient hospital care per stay in the hospital. After this 60 day period the daily coinsurance amount will be $341 for days 61 through 90 and $682 for each lifetime reserve day used. Again, depending on the insurance plan you choose, these deductibles and some coinsurance amounts may be covered by your insurance plan.

Your income is based on your tax return from 2 years prior. Meaning for 2019 Social Security will use your tax return from 2017 to determine your household income. But you may be able to get the high-income surcharge reduced or eliminated if your income has decreased since then because of certain life-changing events, such as the death of a spouse, divorce, retirement or reduced work hours. In that case, you can ask Social Security to use your more recent income instead. Contact the Social Security Administration, estimate your 2019 income, and provide evidence of the change, such as a marriage or death certificate, a signed statement of retirement from your employer, or pay stubs showing your reduced income.nk is external)

Are you retiring in 2019?

There is no cost or obligation for you to talk to me and get the answers to your questions. I welcome all questions and it is my goal to be the single best resource in the state for such questions. And when the time comes for you to enroll in a Medicare Supplement and Prescription Drug Plan, I will help you with that too.

I am a licensed insurance agent working in Maine and New Hampshire. I have contracts with the top health insurance companies available in the area. I am able to help you via email, on the phone, or in person.

If you would like to review your options over the phone or schedule a meeting at your home or office you can reach me at 207-370-0143 or schedule an appointment on my booking website here.(link is external)

“The best part about working with me is that it costs you nothing and you benefit from my full knowledge and experience.”

That’s right. You pay nothing to meet with me. I am paid by the insurance companies in the form of a commission when you enroll in a plan. You pay the same price for the insurance whether you go direct to the insurance company or take advantage of working with someone who has experience and knowledge to help guide you. My goal is to help people and I have found great joy in being able to offer my services to people who need my help.

Would you like my help?

If you would like to talk to me or schedule a meeting at your home or a nearby meeting place, you can reach me at 207-370-0143 or use my simple form on the CONTACT ME page of this site to send an email message. The best part about working with me is that it will not cost you anything to meet with me to discuss your options or to review the plans that are available. I am paid by the insurance companies in the form of a commission if you enroll in a plan. You will not pay any more than anyone else and you are under no obligation whatsoever to enroll in any plans if you meet with me.

“My goal is to help you and I have found great joy in being able to offer my services to people who need my help.”

The Centers for Medicare and Medicaid Services (CMS) has released the 2019 costs for a standard Part D prescription drug plans.

Here are the highlights for the CMS defined Standard Benefit Plan changes from 2018 to 2019. This “Standard Benefit Plan” is the minimum allowable plan to be offered by insurance company who has a contract with Medicare to offer Part D prescription drug insurance.

Initial Deductible:

will be increased by $10 to $415 in 2019.

Initial Coverage Limit (ICL):

will increase from $3,750 in 2018 to $3,820 in 2019.

Out-of-Pocket Threshold:

will increase from $5,000 in 2018 to $5,100 in 2019.

Coverage Gap (donut hole):

begins once you reach your Medicare Part D plan’s initial coverage limit ($3,820 in 2019) and ends when you spend a total of $5,100 in 2019. In 2019, Part D enrollees will receive a 75% discount on the total cost of their brand-name drugs purchased while in the donut hole. The 70% discount paid by the brand-name drug manufacturer will apply to getting out of the donut hole, however the additional 5% paid by your Medicare Part D plan will not count toward your TrOOP (True Out Of Pocket).

For example: if you reach the donut hole and purchase a brand-name medication with a retail cost of $100, you will pay $25 for the medication, and receive $95 credit toward meeting your 2019 total out-of-pocket spending limit.

Enrollees will pay a maximum of 37% co-pay on generic drugs purchased while in the coverage gap (a 63% discount). For example: If you reach the 2019 Donut Hole, and your generic medication has a retail cost of $100, you will pay $37. The $37 that you spend will count toward your TrOOP (True Out Of Pocket).

Minimum Cost-sharing in the Catastrophic Coverage Portion of the Benefit**:

will increase to greater of 5% or $3.40 for generic or preferred drug that is a multi-source drug and the greater of 5% or $8.50 for all other drugs in 2019.

Maximum Co-payments below the Out-of-Pocket Threshold for certain Low Income Full Subsidy Eligible Enrollees:

will increase to $3.40 for generic or preferred drug that is a multi-source drug and $8.50 for all other drugs in 2019.

If you live in Maine or New Hampshire and would like to learn more about the new Medicare plans for 2019 or to go over the changes in your plan, you can call me at (207) 370-0143 or CLICK HERE to send me an email message.

You can also use the BOOK APPOINTMENT(link is external) button below to set up a time to speak with me on the phone or in person. I can also send you information in the mail if you choose.

Have a question that needs to be answered right away? You can talk to a licensed insurance agent by calling (207) 370-0143 or toll free 866-976-9038.

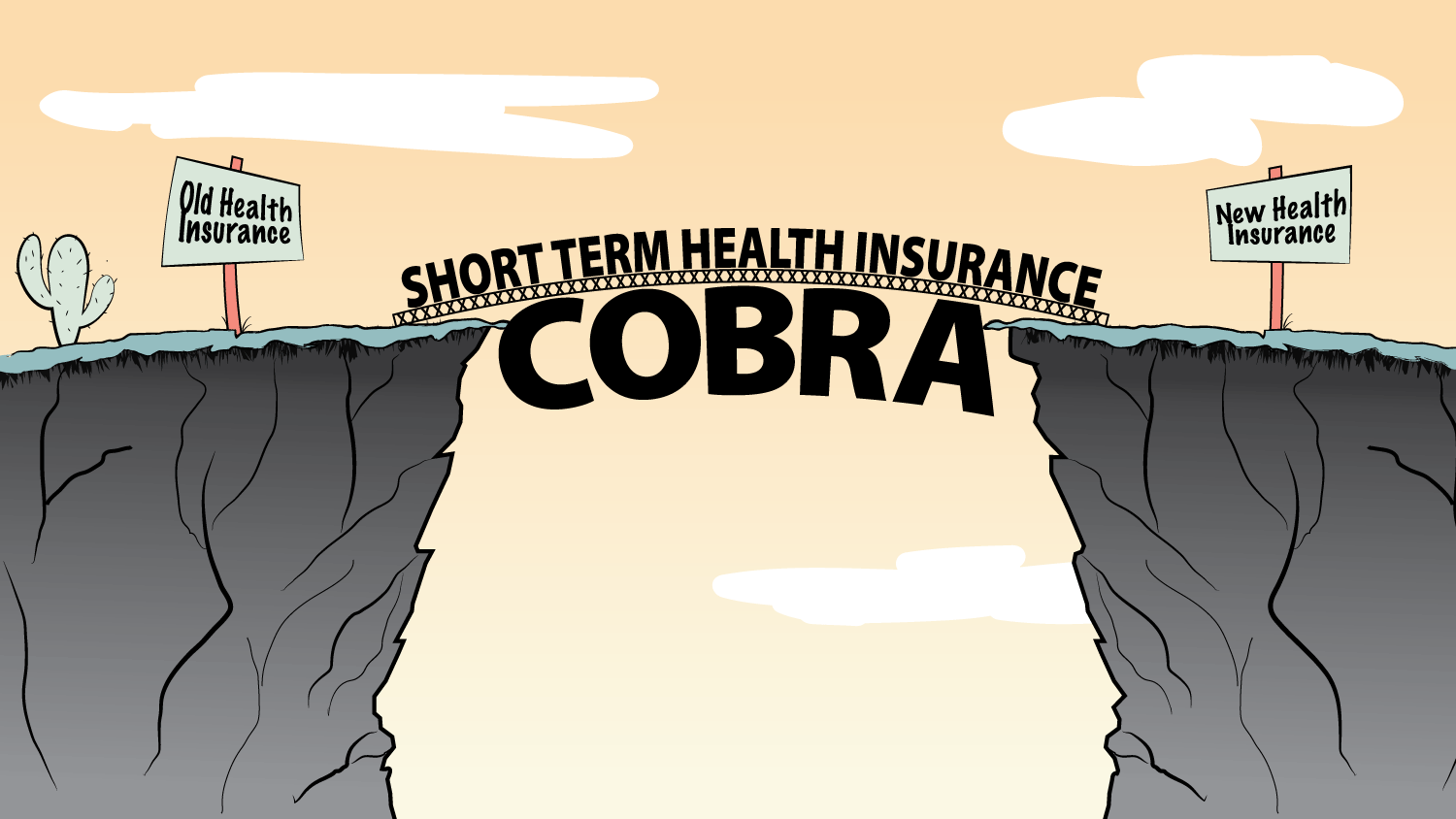

COBRA provides the ability for you and the dependents covered on your health plan to keep coverage after you lose your job or lose coverage for other reasons.

You are eligible for COBRA if your employer’s health plan covers at least 20 employees and you have had an acceptable “qualifying event.”

A qualifying event is something that causes you or your dependents to lost health coverage, such as termination of employment, loss of full-time status, divorce or legal separation, or turning 26 (in the case of your children.)

If you have one of these events, your employer will notify you of your option to enroll in COBRA coverage within 14 days of the plan ending. You will then have 60 days to decide if you want to enroll.

You can keep COBRA coverage for 18 or 36 months, depending on the qualifying event.

In general, COBRA only applies to employers with 20 or more employees.

But, some states require employers covering employers with fewer than 20 employees to let you keep your coverage for a limited time. This is often referred to as “Mini-COBRA” and you can read more about how Maine handles this here: https://www.maine.gov/pfr/insurance/faq/cobra_faqs.html

Your Employer’s Responsibility:

The employer must tell the plan administrator if you qualify for COBRA because of one of these reason:

The covered employee dies

The covered employee lost her/her job

The covered employee becomes entitled to Medicare

Once the plan administrator is notified they must let you know you have the right to choose COBRA coverage.

Your Responsibility:

You or the covered employee are responsible to notify the plan administrator if you qualify because of on of the following reasons:

You’ve divorced or legally separated from the covered employee

You were a dependent child or dependent adult who is no longer a dependent.

You will need to tell the plan administrator about your change in situation within 60 days of the change in order to qualify for COBRA.

COBRA and MEDICARE:

Something really great about COBRA that is not widely known is that if the covered employee becomes entitled to Medicare and the spouse is a few years younger, you do not have to keep working to keep your spouse insured. Your spouse and dependents may keep COBRA for up to 36 months if you lost coverage due to enrolling in Medicare!

You may also keep COBRA coverage for services that Medicare does not cover, such as vision and dental.

You may – for example – if you have COBRA dental insurance, the insurance company that provides your COBRA coverage may allow you to drop your medical coverage but keep paying the premium for the dental coverage as long as you are entitled to COBRA coverage.

If you have Medicare Part A or Part B when you become eligible for COBRA, you must be allowed to enroll in COBRA if you choose. Medicare will be the primary insurance and COBRA will be secondary. You should keep Medicare because it is responsible for paying the majority of your health care costs.

NOTE: COBRA is typically much more expensive than the most expensive Medicare plans so it makes sense to talk to an agent or broker like myself to know your options before you decide to go with COBRA and compare costs.

If you have questions about Medicare or COBRA, you can reach out to me using the CONTACT button on the menu at the top of this website or by calling (207) 370-0143. You can also reach out to the government agencies below.

If you are leaving a government employer contact:

The Benefits Coordination & Recovery Center (BCRC) at 1-855-798-2627.

If you are leaving a private employer contact:

The US Department of Labor at 1-866-487-2365

Maine DOL: (207) 623-7900

New Hampshire DOL: (603) 271-3176

If your employer group health plan coverage was from a state or local government employer then call

The Centers or Medicare and Medicaid Services (CMS) at 1-877-267-2323 extension 61565.

Would you like my help?

If you would like help finding the right plan or just want to ask a few questions, you can call me directly at 207-370-0143 or use my simple form on the CONTACT page of this site to send an email message. The best part about working with me is that it will not cost you anything to talk with me to discuss your options and review the plans that are available. I am paid by the insurance companies in the form of a commission when you enroll in a plan. You will not pay anything to meet with me and you will pay the same price for your insurance that everyone pays whether they had my help or not.

“My goal is to help people and I have found great joy in being able to offer my services to people who need my help.”

More and more of my clients are asking about coverage for vitamins and dietary supplements because their doctors are recommending vitamins and nutritional supplements, such as vitamin D and calcium.

Original Medicare doesn’t cover vitamins and supplements. However some of the insurance plans do offer coverage for them.

If you have a Medigap and a Stand-alone Part D Prescription Drug Plan

Some Medicare Prescription Drug Plans will cover certain vitamins and supplements. Every Medicare Prescription Drug Plan has its own list of covered drugs called a formulary. Check your plans formulary to see what is covered.

In general, Medicare Prescrption Drug Plans will not cover vitamin supplements. But Part D plans that have “enhanced alternative coverage” included in their benefits may include coverage for some vitamins and supplements. Enhanced alternative coverage means the plan’s formulary contains additional items that go beyond the standard Medicare Part D coverage.

You should contact the agent who helped you find your plan to find out if it offers enhanced alternative coverage and what, if any, prescription vitamins and supplements are covered.

A plan’s formulary may change from year to year. Each year you will receive notice of plan changes and it’s a good idea to review those changes and talk to your agent if you have any questions or concerns.

Feel free to contact me if you would like to learn more about your Medicare coverage and options. I am always happy to answer questions.

If you have a Medicare Advantage Plan (MA-PD)

Sometimes referred to as a Part C plan, Medicare Advantage plans have your prescription drug coverage built into the plan. These all-in-one plans also sometimes offer other the counter drug benefits as well as enhanced alternative coverage. To access the over-the-counter (OTC) benefit you usually have a cataloge of covered items, such as vitains, aspirin, cough syrup, antacidis, bandages, cotton swaps and more expensive things like heating pads or incontience supplies.

Generally the plans that offer this type of coverage give you a set dollar amount ($200 per year, $50 per quarter or $25 or $40 per month) and you simply order each month from the catalog and they ship it to free of charge.

If you would like to know if your plan includes these benefits you can give me a call at (207) 370-0143 or reach out to me via email using the CONTACT button on the menu at the top of this webpage.

And if you have any questions about this topic or need help finding a better plan or making a change, I will be happy to help you.

And it won’t cost you anything!

I do not charge anyone the assistance that I provide. I am an independent agent so I don’t work for the insurance company. I work for you. Just like your car insurance agent – I help you search all the different compaies to find the best price and the best coverage. I help you fill out the application and then turn it into the insurance company and follow up on it for you. If there are any difficulties I help you thtough them. Working with me makes Medicare easy!

You can use the BOOK APPOINTMENT(link is external) button below to set up a time to speak with me on the phone or in person. I can also send you information ahead of time to get you started.

Have a question that needs to be answered right away?

If you need to change your Medicare Advantage plan or want to leave your Medicare Supplement or Medigap plan but are worried that you missed the December 7th deadline you can stop worrying right now!

You still have time to make a change!

Medicare’s Annual Election Period (AEP) ended on December 7th – that’s true – but there are some other less commonly known Election Periods or Enrollment Periods during the year that can help you!

This is why I tell all my clients to call me if they need to make a change – no matter what time of year – because there are many opportunities within the Medicare rules and Congress changes these rules every year.

I joke with my clients that, “You don’t have to remember everything I tell you, just remember my phone number!” That usually gets a laugh but it’s absolutely true.

So, how do you keep up with the changes?

You don’t have to. That’s what your insurance agent does!

Each year in the fall Medicare will mail you a copy of the Medicare and You Handbook but some of the information is a year behind because they print it before all of next year’s changes are known.

As part of my job, I keep current on all the changes within the Medicare system and the changes that effect my clients and the Medicare insurance plans and prescription drug plans. I am always reading and researching ways to help people compare and get the coverage they need and find the best plans and best prices.

Starting January 1, 2019 you have a new opportunity to make one change.

If you have a Medicare Advantage plan and need to change to a different plan or if you want to leave your Medicare Advantage plan and return to Original Medicare and get a Medigap plan with a new Part D prescription drug plan you can do this at the beginning of the year.

That’s right. You can still make the changes you need. But you must act quickly because each different plan has a different timeline on when the changes can be made.

The rules and deadlines are different depending on the type of plan you currently have so if you want to call me we can discuss your specific options. My number is (207) 370-0143.

If you want to read more on your own before we talk you can review these new rules on Medicare.gov.

If you would like to talk to me or schedule a meeting at your home of in my office come to my office, you can reach me at 207-370-0143 or use my simple form on the CONTACT page of this site to send me an email message.

The best part about working with me is that it will not cost you anything to meet with me or to discuss your options or to review the plans that are available. I am paid by the insurance companies in the form of a commission – just like your car insurance agent. I get paid by the insurance companies to help you!

My goal is to help people and I have found great joy in being able to offer my expertiese and knowlege to people who need my help.

You can call me at 207-370-0143 or you can book an appointment online – it’s quick and easy!

Here are the Part D changes for 2019 that you need to know!

If your plan has a deductible it may go up. The initial Part D deductible will increase by $10.00 to $415 for 2019.

What does this mean to you?

If your Medicare Part D Rx drug plan has a deductible, you may pay more out-of-pocket in 2019 before your insurance plan begins covering your medications. For example, if you are taking Xarelto which costs about $500 and your plan has a $47 copay then the first refill will cost $462 ($415+$47) and then will be $47 each month after that until you reach the Initial Coverage Limit and enter the “Donut Hole.”

Not all Part D Prescription Drug Plans have a deductible and many plans exclude lower-cost generic drugs from the deductible, giving you coverage for these Tier 1 or Tier 2 drugs before you need to pay your deductible.

Beginning January 1, 2019 your Initial Coverage Limit (ICL) will increase from $3,750 to $3,820.

This means that you will be able to buy slightly more medications before reaching the 2019 Donut Hole or Coverage Gap. A good rule of thumb is that if the full retail cost of your medications is less than $320 per month, you will not enter the Donut Hole before the end of the year.

Good news! The Donut Hole discount will increase 10% in 2019!

The discount you get on brand-name drugs will increase from 65% to 75%. So, if you are using a brand-name medication such as Advair which has a retail cost of around $400, you will pay $100 for your medication or if you take Lantus which has around a $300 price tag, you will pay $75 while in the Donut Hole.

What is the end result?

In 2019 you will have to spend only about $25 more to get out of the Donut Hole than you did in 2018. The Out of Pocket Threshold (or TrOOP) has increased from $5,000 to $5,100 which will trigger entry into the Catastrophic Coverage Phase where you will remain for the rest of the year.

While in the Catastrophic Coverage Phase you will pay either 5% of the total retail cost of the drug OR $8.50 for brand-names and $3.40 for generics, whichever is higher.

If you need a more in-depth explanation of how Part D works or want to review what plans have the lowest costs and will help you avoid the Donut Hole, give me a call. My number is 207-370-0143. I will be happy to help you.

Be sure to read your Annual Notice of Change Letter (ANOC) that should arrive in the mail each year at the beginning of October to see how your plan is increasing – this may help you determine how much you need to budget in 2019 to cover the costs of coverage.[READ MORE …]

If you would like to ask a question or schedule a meeting at your home or a nearby meeting place, you can call me directly at 207-370-0143 or use my simple form on the CONTACT page of this site to send an email message.

The best part about working with me is that it does not cost you anything to talk with me to discuss your options and review the plans that are available. My services are free to you. I am paid by the insurance companies in the form of a commission when you enroll in a plan. You pay nothing for my help!

And you will not pay any more than anyone else and you are under no obligation whatsoever to change your plan if you talk with me.

“My goal is to help people and I have found great joy in being able to offer my services to people who need my help.”

That’s right. You can still make the changes you need. But you must act quickly because each different plan has a different timeline on when the changes can be made.

That’s right. You can still make the changes you need. But you must act quickly because each different plan has a different timeline on when the changes can be made.

My goal is to help people and I have found great joy in being able to offer my expertiese and knowlege to people who need my help.

My goal is to help people and I have found great joy in being able to offer my expertiese and knowlege to people who need my help.

Be sure to read your Annual Notice of Change Letter (ANOC) that should arrive in the mail each year at the beginning of October to see how your plan is increasing – this may help you determine how much you need to budget in 2019 to cover the costs of coverage.

Be sure to read your Annual Notice of Change Letter (ANOC) that should arrive in the mail each year at the beginning of October to see how your plan is increasing – this may help you determine how much you need to budget in 2019 to cover the costs of coverage.