Medicare is a big topic with multiple complexities. Even though you have been paying into it for years, you may know very little about it or how it works. Everyone agrees that it can be difficult to understand the many different insurance plans available and the nuances that go along with each one.

What I do everyday is help people get a better handle on exactly how Medicare works. I explain, in understandable terms, how Medicare works and the different options that you have to best fit your medical and financial situation.

Medicare Part A and Part B

As the song goes, let’s start at the very beginning. Medicare is available to people age 65 or older who are U.S. citizens or who are legal permanent residents, and either you or your spouse have worked for 10 years (or 40 quarters of a year). It is also available to people under 65 with certain disabilities, and people of any age with End-Stage Renal Disease and Lou Gehrig’s Disease (ALS). For details on Medicare eligibility, visit http://www.ssa.gov/medicare.

There are basically two parts to Medicare, Parts A and B. Together, these are also known as “Original Medicare.” If you ever read anything about Medicare in the newspaper or hear about it on TV it is almost always to Parts A and B that they are referring.

Part A: Hospital Insurance

Part A helps cover inpatient care in hospitals, skilled nursing facility care, home health care and hospice care.

Most people do not have to pay a monthly premium for Part A if you or your spouse paid Medicare taxes while working. For this reason, most everyone who is eligible enrolls in Part A when they turn 65 even if they are still working and covered by an employer health plan.

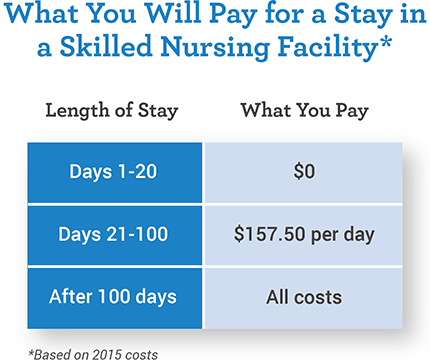

In 2016, there is a $1,288 deductible for the first 60 days that you are and inpatient in a hospital or skilled nursing facility. Medicare calls this your initial “benefit period.” This benefit period resets after 60 days once you are out of hospital care. If you are in the hospital longer than 60 days there is a co-pay of $322 per day up to your 90th day. There is no coverage beyond 90 days each year except 60 days called “lifetime reserve days” that you can use at any time. But understand that once these are used up they are gone for good.

Part B: Medical Insurance

Part B covers your doctor appointments, specialists, outpatient surgeries or care, durable medical equipment, and some preventive services.

Part B differs from Part A in that there is a premium that all beneficiaries must pay each month. The premium starts at $121.80 per month, and can be higher if your annual income is over $85,000 for an individual or $170,000 for a married couple.

Part B also has a $166 deductible, and it will cover about 80% of all costs with no annual maximum out-of-pocket expenses. You pay the remaining 20% as coinsurance.

Additional Medicare Options and Medicare Supplements

If you are enrolled in Medicare Parts A and B, you can choose to buy Medicare Supplement Insurance, known as “Medigap” from a private insurance carrier. There are several plans to choose from and I think it’s best to sit down talk to a professional like myself who has the experience and knowledge to ask the right questions and identify which plans you should consider.

Depending on the supplemental plan that you elect, it will cover some or all of the costs that are not covered by Parts A and B. These programs can also help you cover the uncapped 20% of your medical expenses. There are several Medicare Supplement options that range from Plan A all the way to Plan N.

Typically if your doctor accepts Medicare, he/she will also accept your Medicare Supplement Plan (based on the terms and conditions of the plan). Take important note that neither Medicare nor Medicare Supplement plans cover medications, so you will have to enroll in separate prescription drug plan or Part D plan to cover the cost of your prescription drugs.

Part D- Medicare Prescription Drug Plan

These plans are provided by private insurance carriers. Each plan has their own list of approved drugs (also known as formularies). I carefully review each plan’s list when I meet with new clients to ensure that your medications are covered and more importantly to compare the coverage on each plan to make sure you do not pay too much. The cost for these plans can range from anywhere between $20 to over $100 per month and you can click here to view the plans available.

Part C: Medicare Advantage

Part C is also known as Medicare Advantage. I get asked the most questions about this program. It combines Parts A and B and may add additional benefits (i.e. vision or dental), and typically includes prescription drug coverage (Part D). These plans can be as low as $0 per month in many areas. You can click here to view the plans available in your area. Keep in mind that while using Medicare Advantage Part C, you remain enrolled in both Parts A and B and you are still responsible for those monthly premiums.

Medicare Advantage will generally take the shape of either a PPO or an HMO. A PPO gives you in and out of network choices, while an HMO will give you only one network of providers from which to choose. If you go to in-network providers, you will receive the negotiated rate. Be sure to research the chosen plan’s list of providers to ensure that your doctor is available in that network.

These programs typically have maximum out-of-pocket expenses that can be up to $6,700 per year, not including prescription drugs (in-network). Out-of-network provider expenses can cost even more. However, compared with the prospect of having to pay an “unlimited amount” due to the uncapped 20% we discussed earlier, $6,700 does not sound too terrible.

The Bottom Line

To get the most comprehensive and cost-effective coverage possible, most people end up electing some version of the following two combinations:

- Medicare Part A&B, with a Medicare Supplement Plan and Part D (to cover prescription drugs), OR

- Medicare Part A&B, with a Medicare Advantage Plan (Part C), most of which include Part D (to cover prescription drugs)

- Understand that you will have either a Medicare Supplement Plan or a Medicare Advantage Plan, but not both.

Premium-wise, a Medicare Advantage Plan will typically be less expensive per year than a Medicare Supplement Plan. For example, the cost range of the premium in Maine (my home state) is from $0 to over $110 per month. However, a Medicare Supplement Plan gives you more flexibility as there is no insurance company’s network of doctors that you are required to use. The cost range of the premium in Maine and New Hampshire is generally $100 – $200, depending on your age.

I would suggest that when you are planning for retirement you should also take time to think about your plan for medical insurance.

Would you like my help?

If you would like to talk to me, ask a question or schedule a meeting at your home or a nearby meeting place, you can reach me at 207-370-0143 or use my simple form on the CONTACT ME page of this site to send an email message. The best part about working with me is that it will not cost you anything to meet with me to discuss your options or to review the plans that are available. I am paid by the insurance companies in the form of a commission if you enroll in a plan. You will not pay any more than anyone else and you are under no obligation whatsoever to enroll in any plans if you meet with me.

“My goal is to help people and I have found great joy in being able to offer my services to people who need my help.”

Medicare Advantage Plans May Include Dental

Medicare Advantage Plans May Include Dental Dental discount plans differ in several ways from dental insurance plans:

Dental discount plans differ in several ways from dental insurance plans:

This is where the expertise of an insurance agent like myself can be really beneficial. You can call me and I’ll check all your medications against the plans available and tell you which ones will save you the most. To do this yourself you can use the planfinder tool on Medicare.gov or for the same cost (zero!) you can call me and I’ll help you. 🙂

This is where the expertise of an insurance agent like myself can be really beneficial. You can call me and I’ll check all your medications against the plans available and tell you which ones will save you the most. To do this yourself you can use the planfinder tool on Medicare.gov or for the same cost (zero!) you can call me and I’ll help you. 🙂

Second, nursing homes may wrongly believe that care requiring only supervision (rather than direct administration) by a skilled nurse is excluded from Medicare’s SNF benefit. In fact, patients often receive an array of treatments that don’t need to be carried out by a skilled nurse but that may, in combination, require skilled supervision. In these instances, if the potential for adverse interactions among multiple treatments requires that a skilled nurse monitor the patient’s care and status, then Medicare will continue to provide coverage.

Second, nursing homes may wrongly believe that care requiring only supervision (rather than direct administration) by a skilled nurse is excluded from Medicare’s SNF benefit. In fact, patients often receive an array of treatments that don’t need to be carried out by a skilled nurse but that may, in combination, require skilled supervision. In these instances, if the potential for adverse interactions among multiple treatments requires that a skilled nurse monitor the patient’s care and status, then Medicare will continue to provide coverage.

While the review is being conducted, the patient is not obligated to pay the nursing home. However, if the appeal is denied, the patient will owe the facility

While the review is being conducted, the patient is not obligated to pay the nursing home. However, if the appeal is denied, the patient will owe the facility

The term first was coined during a 1938 political campaign as a euphemism for “old person,” and now enjoys widespread usage in the common vernacular, legislation, and business. Some dictionaries define “senior citizen” as a person over the age of 65. In everyday speech, the term is often shortened to “senior.”

The term first was coined during a 1938 political campaign as a euphemism for “old person,” and now enjoys widespread usage in the common vernacular, legislation, and business. Some dictionaries define “senior citizen” as a person over the age of 65. In everyday speech, the term is often shortened to “senior.”