Did you choose the wrong plan last fall?

Did you choose the wrong plan last fall?

You may qualify for a second chance to correct the mistake!

How can you Change your Medicare Advantage Plan?

There are a lot of rules around when you can change your Medicare Part C or Medicare Advantage Plan.

Most people know that you can enroll in or leave a Medicare Advantage Plan during the Annual Open Enrollment Period in the Fall which starts October 15 and ends December 7 each year.

What most people don’t know is …

You can also leave your Medicare Advantage Plan (Part C) and go back to Original Medicare (Parts A & B) during the first 6 weeks of the new year. This is called the Medicare Advantage Dis-enrollment Period.

You can only make this coverage change if you have a Medicare Advantage Plan.

This Disenrollment Period occurs every year from January 1 to February 14.

And changes made during this period will become effective the first of the following month. For example, if you switch from a Medicare Advantage Plan to Original Medicare in February, your new coverage will begin March 1.

Why would you want to go back to Original Medicare?

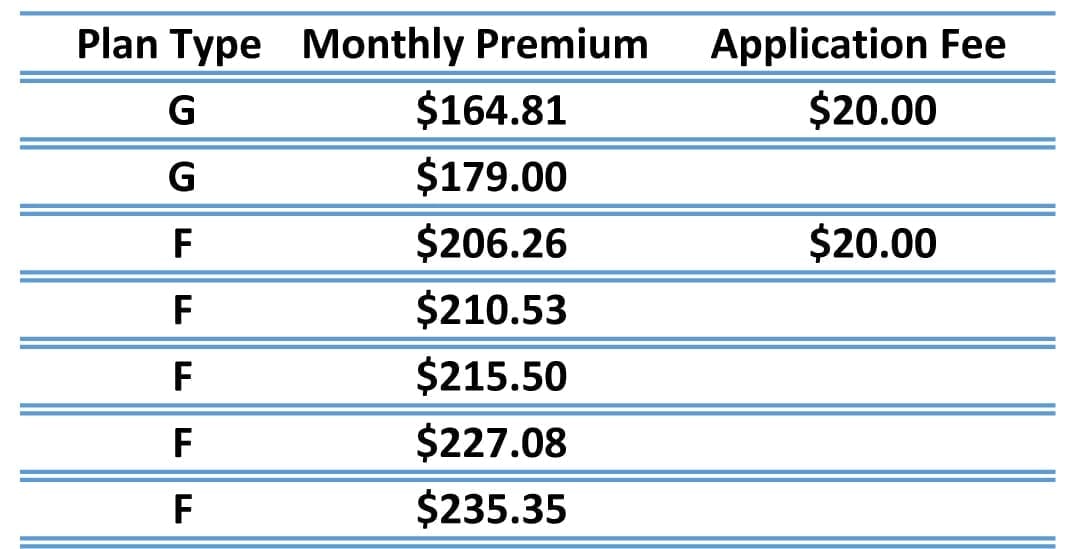

Medicare Supplement plan benefits are standardized, which means Plan F is Plan F and Plan G is Plan G. No matter which insurance company you choose to provide this plan the coverage is the same. But they all charge a different price. [READ MORE…]

Perhaps your Medicare Advantage plan has some costs you were not aware of when you signed up or your plan changed this year. Some of these changes may include; higher deductibles, higher monthly premiums, new restrictions on doctors, hospitals, and pharmacies that are different from last year.

Perhaps your Medicare Advantage plan has some costs you were not aware of when you signed up or your plan changed this year. Some of these changes may include; higher deductibles, higher monthly premiums, new restrictions on doctors, hospitals, and pharmacies that are different from last year.

Sometimes the cost of your prescription drugs may have increased or your anticipated costs of health care and hospital services has gone up. If you find you’re going to physical therapy or seeing a doctor more often then you may be paying a lot more out of pocket and this might increase as you get older.

Since Medicare Advantage plans are completely administered through a private insurance company, the rules and guidelines can vary between plans and from year to year, which can lead to restrictions like these:

Since Medicare Advantage plans are completely administered through a private insurance company, the rules and guidelines can vary between plans and from year to year, which can lead to restrictions like these:

Your Medicare Advantage plan may require higher out-of-pocket costs than with Original Medicare and these may increase each year as your health needs change.

The insurance company may require you to follow stricter rules to get coverage for certain services or health products, like getting referrals to see specialists or getting prior authorizations that delay necessary tests. You may also have to change your doctor or hospital to one within the new plan’s network, or you may have to pay a higher cost.

If you want to change, you can. You just have to know when.

If you missed the February 14th deadline for the Dis-enrollment period, there are also certain circumstances that would make you eligible for a Special Enrollment Period (SEP) to change your health and or drug plan outside of the usual enrollment or dis-enrollment periods.

If you qualify for a Special Enrollment Period, you may leave your Medicare Advantage Plan and your new Medigap or Supplement plan will start the first of the month after you sign up for or dis-enroll from the Medicare Advantage Plan.

One example of when you qualify for an SEP: when your Medicare Advantage Plan leaves your area or you move out of your plan’s service area, you can switch to another Advantage plan or go back to Original Medicare and get a Medicare Supplement. Remember to enroll early during any enrollment period to make sure that your new coverage starts when it should.

If you have any questions about this or need help making a change, I will be happy to help you.

And it won’t cost you anything!

I do not charge anyone for my help, whether you enroll with me or not. I get paid by the insurance company when I deliver your application so once we pick the right plan I will help you fill out the application and I will turn it into the insurance company for you. It doesn’t get any easier than that!

What do you have to do?

What do you have to do?

If you live in Maine or New Hampshire and would like more answers or if you’re looking for help choosing a Medicare plan or just have some questions, I would be more than happy to help you.

If you live in Maine or New Hampshire and would like more answers or if you’re looking for help choosing a Medicare plan or just have some questions, I would be more than happy to help you.

It will not, however, pay for any follow-up dental care after the underlying health condition has been treated. So, if Medicare paid for a tooth to be removed as part of surgery to repair a facial injury, do not expect Medicare to pay for any other dental care you may need later because you had the tooth removed, and Medicare will not pay for dental implants or dentures to replace the extracted tooth.

It will not, however, pay for any follow-up dental care after the underlying health condition has been treated. So, if Medicare paid for a tooth to be removed as part of surgery to repair a facial injury, do not expect Medicare to pay for any other dental care you may need later because you had the tooth removed, and Medicare will not pay for dental implants or dentures to replace the extracted tooth.

Some Medicare Advantage Plans Include Dental Coverage

Some Medicare Advantage Plans Include Dental Coverage

If not, you will have seven months to contact your nearest Social Security office and enroll in Medicare. Your initial enrollment period starts three months before the month you turn 65, the month you turn 65, and three months after, totaling seven months.

If not, you will have seven months to contact your nearest Social Security office and enroll in Medicare. Your initial enrollment period starts three months before the month you turn 65, the month you turn 65, and three months after, totaling seven months.

Be sure to read your Annual Notice of Change Letter (ANOC) that should arrive in the mail each year at the beginning of October to see how your plan is increasing – this may help you determine how much you need to budget in 2018 to cover the costs of coverage. [

Be sure to read your Annual Notice of Change Letter (ANOC) that should arrive in the mail each year at the beginning of October to see how your plan is increasing – this may help you determine how much you need to budget in 2018 to cover the costs of coverage. [

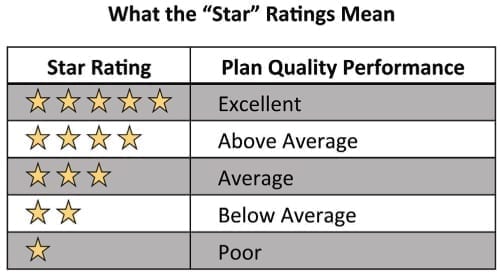

Last week, I was parked in a parking lot, returning phone calls in between appointments and saw these seagulls flying around foraging for food.

Last week, I was parked in a parking lot, returning phone calls in between appointments and saw these seagulls flying around foraging for food. Sure enough, after a while the solo gull discovered a treasure trove of something tasty nearby a dumpster.

Sure enough, after a while the solo gull discovered a treasure trove of something tasty nearby a dumpster. Likewise, just because Medicare rates one plan higher than another, that ALSO does not mean it’s the best one for you.

Likewise, just because Medicare rates one plan higher than another, that ALSO does not mean it’s the best one for you.

Who gets one and what should you do with it?

Who gets one and what should you do with it? Fall Open Enrollment runs from

Fall Open Enrollment runs from

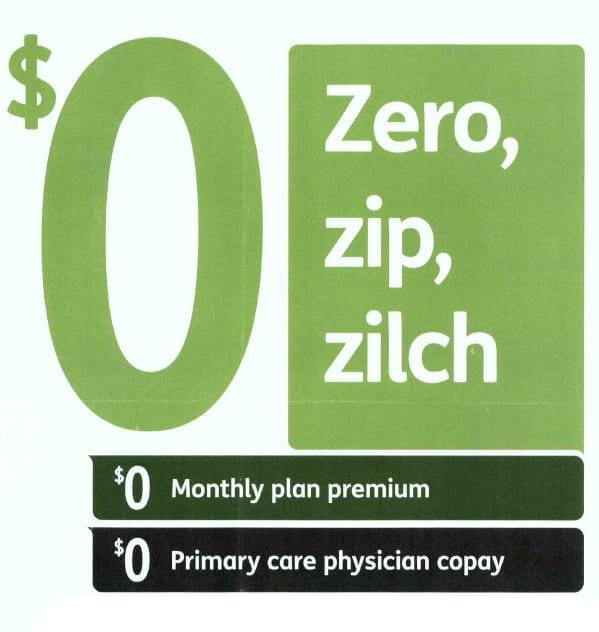

$0 Premium Medicare Advantage Plans do actually cost you nothing per month for the insurance plan and they also often times offer other services or generic prescriptions for $0 but these plans are not actually free.

$0 Premium Medicare Advantage Plans do actually cost you nothing per month for the insurance plan and they also often times offer other services or generic prescriptions for $0 but these plans are not actually free. However, $0-premium Medicare Advantage plans might not always be the most affordable option.

However, $0-premium Medicare Advantage plans might not always be the most affordable option.