Part D Explanation of Benefits

Understanding Your Part D Explanation of Benefits

Here is how to read and use this helpful drug benefit summary.

You get a lot of mail from Medicare & your insurance. One document to watch for is your monthly Medicare prescription drug plan “Explanation of Benefits” (EOB).

Think of your EOB as a helpful tool for managing your Part D prescription drug claims and costs.

It’s important to review your Part D Explanation of Benefits!

This document provides a summary of the prescriptions you’ve filled in the previous month and information about your drug coverage, such as:

- Whether you’ve met your deductible (if you have one) and, if not, how much more you need to spend before your plan begins to pay its share.

- What you have paid “out-of-pocket” to date for your prescriptions.

- Which Part D coverage stage you are in

How to Read Your EOB

The first page contains a list of the six sections of information it provides. Let’s take a look at the first three sections in detail.

SECTION 1: Your prescriptions in the last month

- Chart 1 shows a list of your prescriptions filled by date in the past month and which pharmacy you used. Be sure to check the accuracy of this list.

- The chart displays three columns that show the amount the plan paid, what you paid, and any other payments from an organization or a program like a State Pharmaceutical Assistance Program (SPAP).

Near the bottom of the chart, you’ll see the monthly totals paid for your prescriptions. This total will include what was paid by the plan, by you, and by other programs on your behalf, if any.

The information will be identified as “total drug costs”. The section will also provide your monthly out-of-pocket costs. At the bottom, you can view the year-to-date total for what you’ve spent out of pocket on prescriptions. Finally, a total of the three columns indicates what you, your plan, and other organizations, if any, have spent since January 1. This information will be identified as “year-to-date total drug costs”.

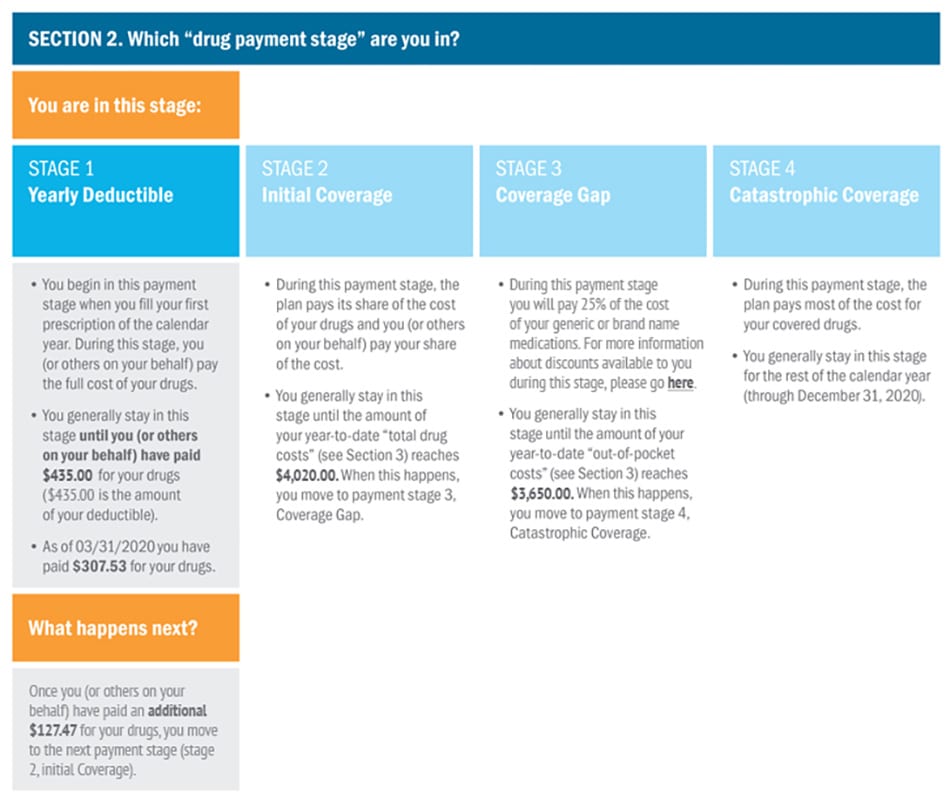

SECTION 2: The Part D drug payment stages

In this view, the stage you’re in is identified by a shaded outline—for more information on the stages of coverage, please go here. Here you will see a description of the dollar amount you and/or your plan need to reach before moving to the next stage of coverage. This information will be identified as “total drug costs”. It will also show your current year-to-date “total drug costs,” which indicate how close you are to moving to the next stage of coverage.

The bottom section of the shaded box “What happens next?” gives you the additional amount that you, your plan and others on your behalf (if any) need to spend in “total drug costs” to move to the next payment stage.

This is especially important if you are in the Initial Coverage stage, because you will see how close you are to entering the Coverage Gap (aka Donut Hole), when you will pay more for your prescriptions.

Before you get too close to the gap, you might want to review your medications with your insurance agent or broker to see what you will pay Ask if there are ways to delay entering this stage, such as by switching to a generic medication or using a coupon or Patient Assistance Program.

SECTION 3:“Out-of-pocket” and “total drug costs” amounts and definitions

This section provides your monthly and yearly“out-of-pocket costs” and “total drug costs” along with definitions of what these costs include or do not include.

Additional Information

The last three sections provide information on various topics.

Section four may include changes to your Drug List that affect drugs you take, such as a change to the coverage or cost of a drug.

Section five tells you what to do if you find a mistake in the EOB or have questions.

Additionally, you can find information about protecting yourself from fraud and how to contact the plan or Medicare with your concerns. Section six discusses the plan’s Evidence of Coverage, the benefits booklet that explains the plan and the rules you need to follow to obtain drug coverage. Certain chapters and topics are highlighted that will provide you with instructions if you have issues related to your drug coverage or difficulty paying for your drugs

Want to know more? I can help!

If you would like help finding answers to your questions, you can call me directly at 207-370-0143 or use my simple form on the CONTACT page of this site to send an email message. I am always happy to help!

The best part about working with me is that it costs you nothing! I am paid by the insurance companies in the form of a commission when I enroll someone in a plan. This is the same way it works when you buy car insurance or your home owners insurance. You do not pay anything to the agent and you will pay the same price for your insurance that everyone pays whether they had my help or not.

“My goal is to help people and I have found great joy in being able to offer my services to people who need my help.”

Triple Tax Advantage of HSAs

Triple Tax Advantage of HSAs